Corporate Insolvency. Why has there not been more?

Corporate Insolvency. Why has there not been more?

ij Member Mark Homan of the firm BHSM, Dublin, discusses the surprising lack of anticipated corporate insolvencies due to the global Coronavirus Pandemic and gives his insight on why this is so.

Corporate Insolvency. Why has there not been more?

With the early onset of the Coronavirus Pandemic, it had been widely anticipated that corporate insolvencies would increase exponentially as businesses suffered from a sharp decrease in revenue with a knock-on effect on their ability to meet their credit obligations. For many reasons, explored below, in the main this has not transpired to be the case. This article explores some of the reasons why. Whilst this article is from an Irish viewpoint there are many similarities across many other countries, particularly in developed economies.

Strong Macro-Economic Conditions

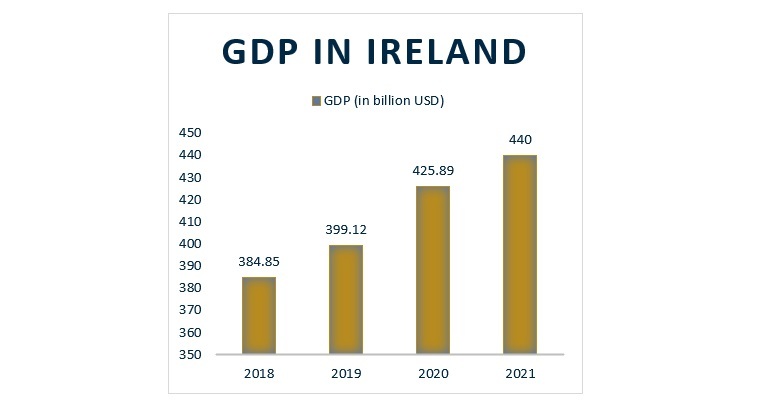

Interestingly, GDP statistics from the World Bank show that despite the effects of a Global Health Pandemic, Ireland (like many other counties) did not go into a recession as many expected. On the contrary, Ireland continues to grow its economy despite the challenges presented by COVID-19. GDP in Ireland in 2018 was 384.85 billion US Dollars. It was 399.12 billion US Dollars in 2019 and in 2020 it increased to 425.89 billion US Dollars. This represents a growth of 3.4% between 2019 and 2020. GDP has continued to increase in 2021 and is expected to reach 440 billion US Dollars by year end.

Strong macro-economic growth has also been represented in recent exchequer figures. Corporation tax receipts in 2021 amounted to €4 billion, which was 31% higher than in November the previous year. November 2021 VAT receipts were strong at €2.6 billion which is nearly 25% higher than in the same period in 2020. These figures indicate the continued strength of Ireland’s economic performance and bely the strains that have been placed on the economy arising out of the Pandemic.

Unprecedented Government Supports Available

Whilst the economy continues to perform well, this is misleading as many businesses have suffered extreme trauma, particularly those for example in hospitality and retail. Businesses which would ordinarily have become corporate casualties, have only survived because of Government Supports.

The Irish Government, like many, were quick to roll out unprecedented State support. In Ireland some of the measures included:

A Temporary COVID-19 Wage Subsidy Scheme (TWSS) from March 2020 to August 2020. TWSS enabled employers that were affected by the pandemic, to receive significant supports towards the cost of salaries. The driver for this initiative was to keep people in work. This was then continued by an Employment Wage Subsidy Scheme (EWSS) which provided a flat-rate subsidy to qualifying employers. EWSS had the effect of shielding many businesses against the cost of redundancies which may otherwise have resulted in their insolvency.

A Pandemic Unemployment Payment (PUP) was also introduced as a social welfare payment for employees and self-employed people who had lost all of their income from employment due to COVID-19.

Debt Warehousing was introduced by the Tax Authorities. This was a key measure designed to support companies and avoid their insolvency. The Scheme allowed businesses to warehouse tax debts such as Value Added Tax (V.A.T.) and PAYE (Employer) liabilities. This measure was key to Companies maintaining cash flow, particularly during lock down periods.

Freezing of commercial rates payable by businesses to local government, in respect of their business premises.

Government backed loans to businesses were introduced. For example, in 2020 the government introduced a €2 billion COVID-19 Credit Guarantee Scheme to provide Irish businesses, including those in the farming and fishing sectors, with access to low-cost loans as they respond to the impacts of COVID-19. This was the largest ever state-backed loan guarantee scheme in Ireland.

Other Factors

Many of the businesses affected by COVID-19 are tenants in commercial leases. Generally speaking, there has been forbearance shown by Landlords towards struggling commercial tenants.

The Irish Government also introduced a voluntary Code of Conduct between Landlords and Tenants. The Code, which is a commitment in the Programme for Government, has been developed in consultation with landlords and business representatives for commercial tenants. It is based on an approach taken in other jurisdictions, including Australia, France and the UK. It sets out a structured approach for engagement between both commercial landlords and tenants, based on their mutual interest in continuing to work together.

Additionally, the Irish Government have amended / introduced legislation in an effort to support businesses and to protect them against creditors (for example increasing the amount in respect of which a creditor can seek the winding up of a Company on the basis of its insolvency).

The Effect of these Supports and Other Factors

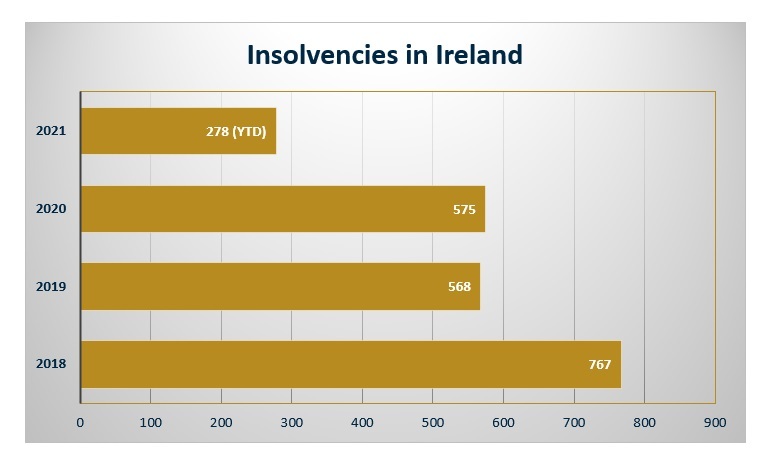

Broadly speaking, the effect of the aforementioned supports is that the expected increase in corporate insolvencies has not come to pass. According to insolvency statistics published by Deloitte, the total number of insolvencies in 2018 was 767. The total number recorded in 2019 and 2020 was 568 and 575, respectively. The number of corporate insolvencies recorded in Ireland year-to-date (YTD) as of 30 September 2021 stands at 278. This represents a substantial decrease of 36% from the same period in 2020, when the total number recorded was 431. It is clear that rather than the expected increase, there has in fact been a decrease in the number of insolvencies.

The table above is proof that the Global Pandemic, in Ireland (and in many other countries) has not resulted in the expected avalanche of corporate insolvencies.

The Effect on Litigation and Transactions from a Legal Practice Perspective

Typically, in a recession or general downturn in trade, legal practices see a downturn in transactions and an uptick in litigation. For the reasons set out above this has not turned out to be the case. The reasons listed below are some additional contributory factors:

The Legal system has typically been a slow adaptor to technology, so its infrastructure is limited in terms of the case load it can manage. Many cases were put on hold for extended periods, and whilst there are some remote hearings taking place, capacity levels are reduced.

On the other hand, after an initial period of uncertainty, M&A activity has been at record high levels. This can probably be attributed to a sustained period of all time low interest rates and an abundance of Private Equity funding.

It is worth pointing out that whilst litigation is only beginning to move towards pre pandemic levels, advisory work has remained strong throughout, particularly in the areas of employment and landlord and tenant related issues.

What do we expect for 2022?

Approaching the latter end of 2021, it had been widely predicted that there would be a phased reduction in governmental supports which would inevitably lead to an increase in insolvencies. However, with the continued presence of COVID-19 and the new Omicron variant (and other possible variants), the Irish Government is under pressure to continue with supports. The Revenue Commissioners will also be expected to provide further forbearance.

New measures have been introduced, with legislation recently enacting the Small Company Administrative Rescue Process (SCARP) which provides a more accessible and cost-effective alternative to examinership for Small and Micro Enterprise’s (SME). This may result in the restructuring of Small and Medium Size businesses, but ironically it may not be until the end of this unprecedented Global Health crisis and the ensuing withdrawal of Government supports that we see the full impact on businesses.

How We Can Help

If we can be of any assistance or address any general queries you may have, please do not hesitate to contact Mark Homan mhoman@bhsm.ie / +353 (0)1 440 8300.

This article is for general information purposes. Legal advice must be obtained for individual circumstances. Whilst every effort has been made to ensure the accuracy of this article, no liability is accepted by the author for any inaccuracies.